What is so special about this Silicon Valley? Why build startups specifically in the American market?

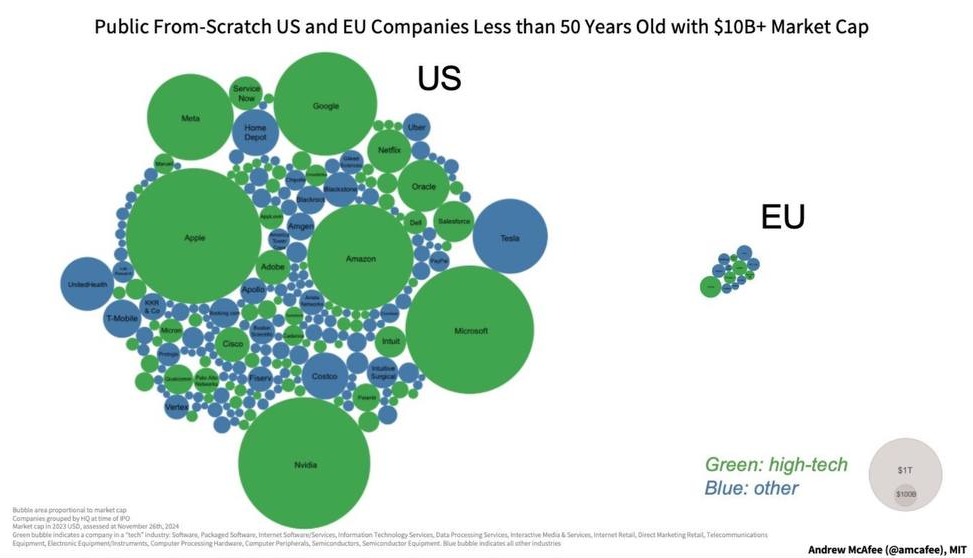

If you look at a chart of US versus European company valuations (only companies above $10B are shown), the difference is striking.

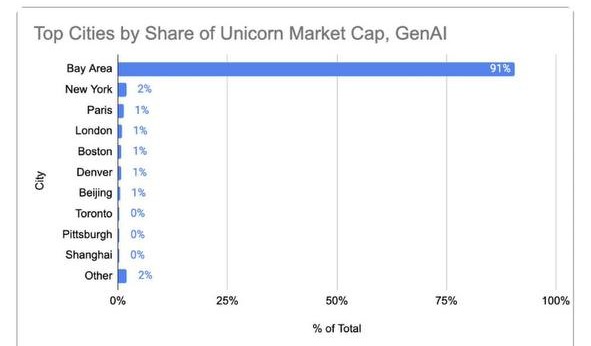

In AI specifically, the imbalance is even sharper. The Valley concentrates 91% of AI companies (by market cap). Data: CBInsights.

The chart is saying that if your AI startup is in, say, even New York, you will never raise a round of the right size from the right investors, you won't be able to grow fast enough, and your company will never be valued at the same level as a full analog in the Valley. Period.

It's pointless to argue whether we like this state of affairs. I don't either. But it's objective reality. You don't win arguments with reality. Of course, this is a market phase and a bubble. But in another phase the share would be 81%, not 91%. That doesn't change the point.

Where does this concentration of capital come from?

The reasons are clear. If the money printer is in the US, then most of the money will settle in the US: with buyers, with strategic acquirers (those who buy the businesses themselves), with venture funds (who get it from pension funds), and ultimately on the stock market after IPO (from all other institutional players). Money never sleeps, pal.

A couple of examples from my own experience.

Strategic buyers — 50x more

The picture will be the same in any industry. I looked at online education as an example. In edtech, over the previous 3 years, 150 different strategic buyers acquired edtech companies. In Russia, in the same period, there were 2. A 75x staggering difference. Makes total sense, given the size of the economy.

Multiples — 10x higher

A gaming company with $50M run rate (not revenue) and a loss is bought by a US strategic acquirer for $500M. That's 10x multiple to revenue and an 'infinity' multiple to profit.

A gaming company based in Russia with $2.5M monthly revenue ($30M run rate) and 50% EBITDA margin (profit forecast of $15M) is bought for $30M. The revenue multiples' difference is 10x. Same business, different conditions. The valuation gap has grown even wider since.

Demand — 50x higher

The picture varies by industry. In edtech, I remember running parallel negotiations with a top-10 Russian company (60,000 employees) and a small Texas call center of 40 people. The Texans were ready to pay more for the same product (something like "$1,000 per person, sure, sounds OK for a yearly subscription") and, frankly, drained my brain less.

What should a founder do?

A young founder walks into a poker hall. The skills required at different tables are absolutely the same. The concentration of energy and effort required is also the same — total obsessive focus for 7–10 years, with no chance to step out into the daylight and breathe fresh air.

It's just that some tables are stacked with chips and others aren't. Which table should you pick? In my view, it's a no-brainer.

Every attempt to get into Indonesia or Brazil hits the question: "And to whom exactly are you planning to sell this? At what valuation?"

The end of the dollar era (on a 7–10 year horizon) will change this state of affairs. But for now, that's the reality.